The Great Debate: Credit Cards vs Debit Cards for Everyday Spend

I’m Brian Olson, a cybersecurity professional with deep experience in DFIR and network forensics—currently working in Big Tech. My mission? To share hard-won lessons not just with fellow experts, but with anyone learning and growing in security—especially those in smaller companies without the resources or teams a massive enterprise has. I started blogging to break down real-world strategies, honest tool reviews, and battle-tested workflows in plain language. Whether you’re an underdog SOC analyst or a curious IT pro tackling security for the first time, my goal is to make the practical side of cybersecurity a little less overwhelming—and a lot more actionable. Expect guides that cut through the noise, resources that are actually useful at the keyboard, and stories that prove you don’t need a giant budget to make a real impact. You’ll also find my takes on personal finance, real estate, and anything that helps us level up—in and out of work. Let’s connect. We’re all in this together!

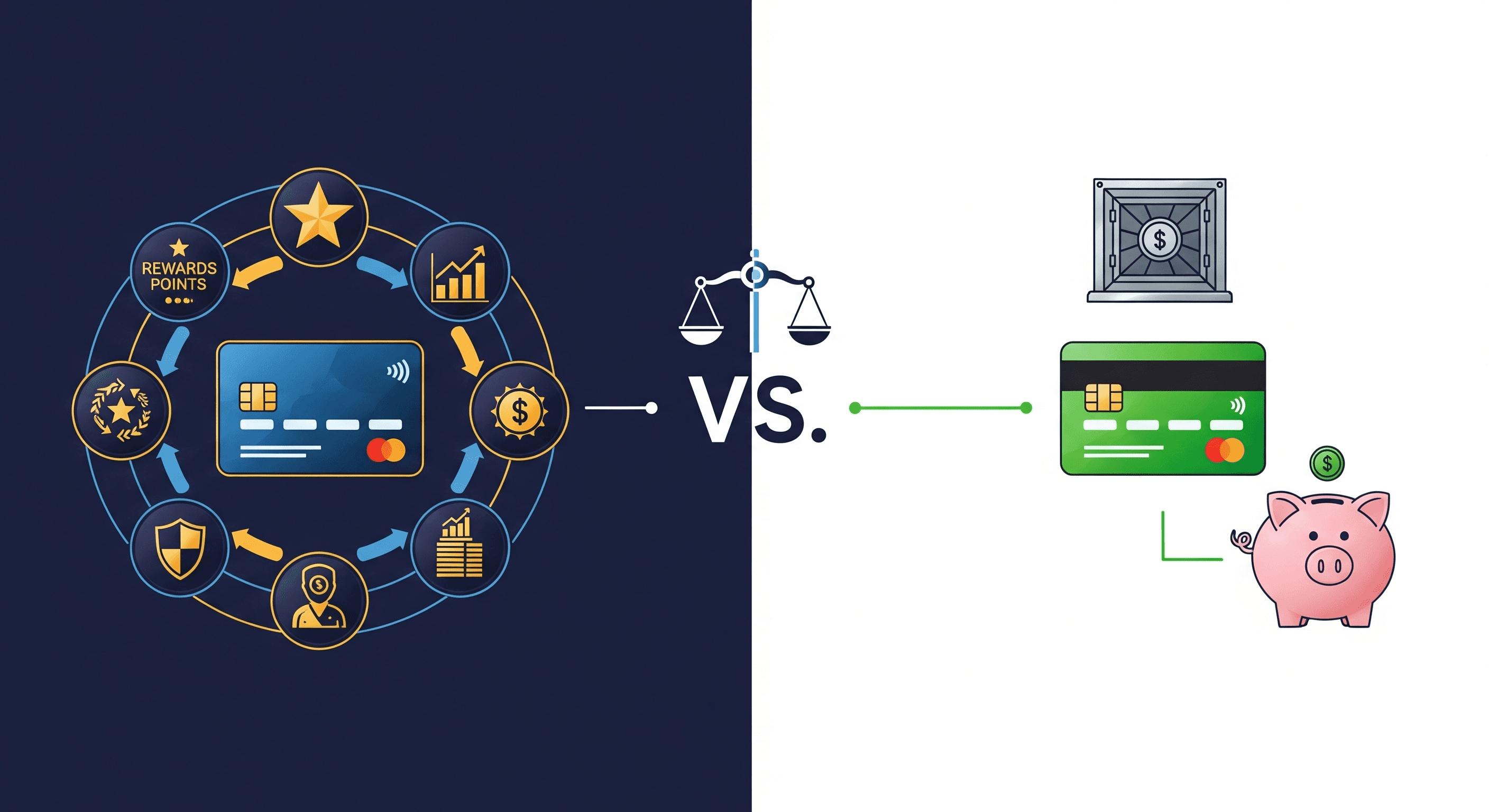

In today’s digital age, the way we manage our finances has changed dramatically. Gone are the days of cash-only transactions; now, we have a plethora of payment options at our fingertips. Two of the most popular choices are credit cards and debit cards. But which one is best for everyday spend? In this post, we’ll delve into the pros and cons of each option to help you make an informed decision.

Credit Cards: The Pros and Cons

Credit cards offer a range of benefits, including:

Rewards and cashback: Earn points or cashback on all your purchases, redeemable for statement credits, gift cards, or travel.

Convenience: Credit cards are widely accepted and eliminate the need to carry cash.

Purchase protection: Enjoy protection against lost, stolen, or damaged items.

Building credit: Using credit cards responsibly can help establish or improve your credit score.

Travel benefits: Many credit cards offer travel-related perks, such as airport lounge access or travel insurance.

However, credit cards also come with some drawbacks:

Overspending: The temptation to overspend can lead to debt and financial difficulties.

Interest charges: If you don’t pay your balance in full each month, you’ll incur interest charges.

Fees: Annual fees, late fees, and foreign transaction fees can add up quickly.

Debt accumulation: Using credit cards for everyday spend can lead to debt accumulation if you’re not careful.

Debit Cards: The Pros and Cons

Debit cards, on the other hand, offer:

Budgeting control: Debit cards draw directly from your checking account, helping you stick to your budget.

No interest charges: You won’t accumulate debt or incur interest charges.

No fees (usually): Most debit cards don’t have annual fees, late fees, or interest charges.

Simple and convenient: Debit cards are widely accepted and easy to use.

No credit score impact: Debit card usage doesn’t affect your credit score.

However, debit cards also have some limitations:

Limited protection: Debit cards often have limited protection against unauthorized transactions or disputes.

No rewards or cashback: Unlike credit cards, debit cards rarely offer rewards or cashback.

No purchase protection: You’re responsible for lost, stolen, or damaged items.

Overdraft fees: If you’re not careful, you might incur overdraft fees if your account balance is low.

The Verdict

So, which one is best for everyday spend? The answer depends on your individual financial situation and goals. If you’re careful with your budget and don’t need the benefits of credit cards, debit cards can be a suitable choice. However, if you want to earn cashback or rewards, enjoy purchase protection, or build credit, credit cards might be the better option (my preference).

Best Practices for Using Credit Cards and Debit Cards

Regardless of which option you choose, here are some best practices to keep in mind:

Pay your balance in full: If you’re using a credit card, pay your balance in full each month to avoid interest charges. Interest charges will quickly destroy the value of cashback or rewards.

Set a budget: Track your expenses and set a budget to avoid overspending. I like the tool Monarch Money, which I wrote about here.

Choose a card with no fees: Select a credit card or debit card with minimal fees.

Monitor your credit score: Regularly check your credit score to ensure it’s not negatively impacted by your credit card usage.

In conclusion, both credit cards and debit cards have their advantages and disadvantages. By understanding the pros and cons of each option and following best practices, you can make an informed decision about which one is best for your everyday spend.